Are the strong returns of the S&P 500 a reflection of the growth in the U.S. economy?

Global Investment Strategist

The debate as to whether the S&P 500, an index of 500 large-cap companies in the U.S., reflects the overall growth in the U.S. economy will probably never be settled. Equity markets are, by nature, forward looking in a way that economic data cannot be. Investors can imagine what capital expenditures (capex) may take place well before that capex actually gets reflected in the economic data. But the first half of 2025 seems to be an interesting point in time where the equity markets and the overall economic statistics are reflecting a very similar reality – that the buildout of the ecosystem around artificial intelligence (AI) is a dominant driver of both the growth in the U.S. economy and equity market returns.

AI capex spending the bright spot in first-half GDP data

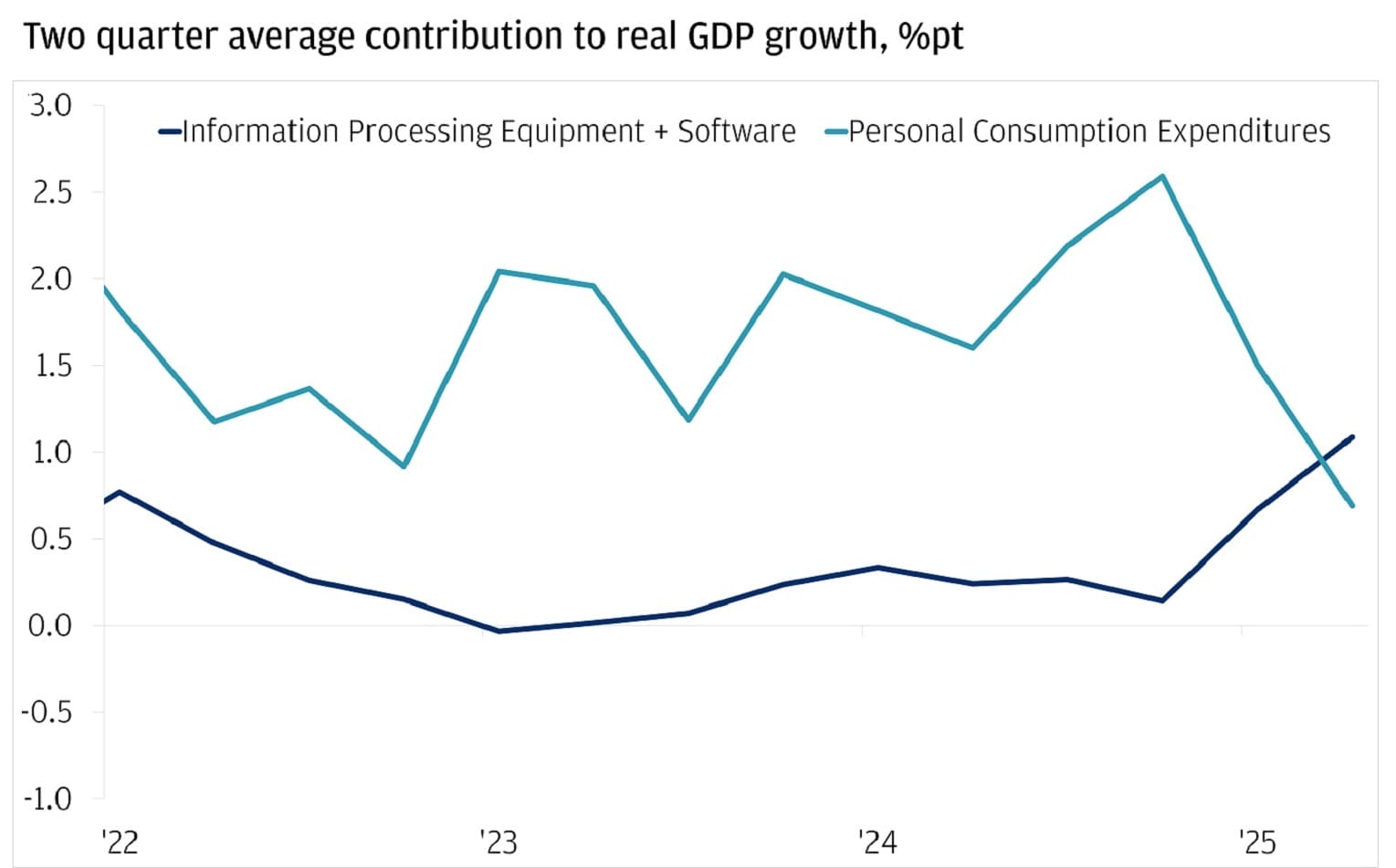

A funny thing happened in the first half of 2025 in the GDP statistics. Investment in information processing equipment and software, essentially AI and AI-adjacent investments, contributed more to real GDP growth than personal consumption. Given how much larger consumption is as a share of the economy in dollar terms, this essentially means that the growth rate in AI capex boomed while growth in personal consumption was relatively weak. It’s clear that the pickup in AI capex was the bright spot during the first half of the year as economic growth slowed to a 1.4% annualized pace, down from the 2.5% pace in 2024.

AI investment contributed more to growth than consumption in H1 2025

Ready to take the next step in investing?

We offer $0 commission online trades, intuitive investing tools and a range of advisor services, so you can take control of your financial future.

Data center construction is booming

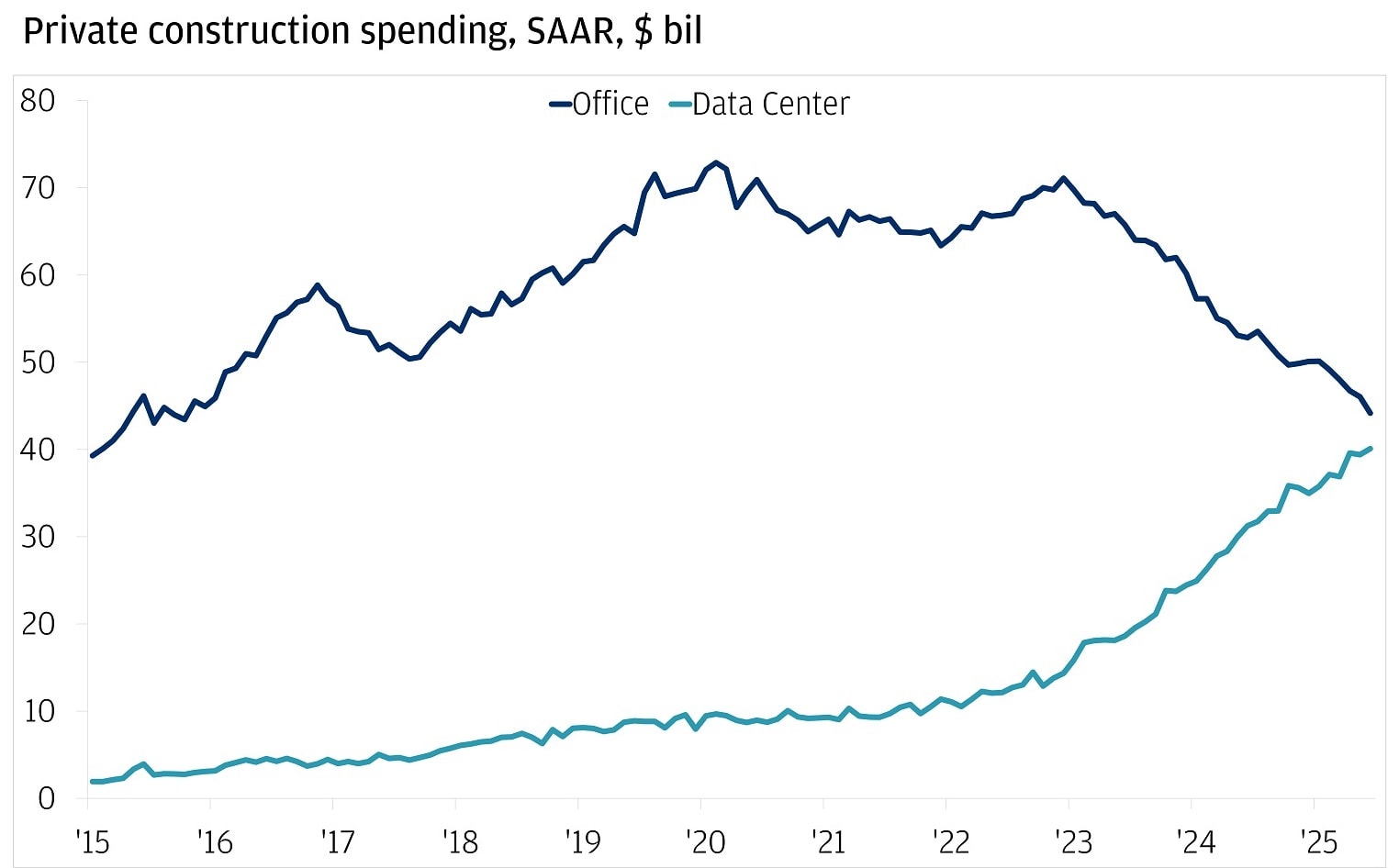

The strength of AI capex is also corroborated in the U.S. private construction data. As the chart below shows, annualized data center construction spending is rapidly approaching the same amount that is spent in the U.S. on office construction.

Data center construction is booming

It’s a meaningful shift from even just a few years ago as the development of the AI ecosystem ramps up in line with AI adoption rates continuing to trend higher. In a survey conducted by the Census Bureau, the percent of businesses responding that they expect to use AI to produce a good or service in the next six months has increased from roughly 6% when the survey began in September 2023 to 13% as of August 2025. As adoption rates continue to rise, it’s no surprise that companies are investing heavily in infrastructure capacity – everything from physical data centers to heating, ventilation and air conditioning (HVAC) systems to cool said data centers – to eventually handle the higher demand.

Outside of AI, capex intentions are relatively muted

Interestingly, this capex acceleration is not expected to meaningfully spill over across the economy. For one, the previous chart shows that the construction of offices continues to trend lower. Residential housing construction doesn’t look much better, and when we examine capex expectations across the economy, we see they are 1 standard deviation below average. Looking ahead, the potential for lower interest rates and new tax incentives in 2026 could lead to a pickup in capex intentions, but that is yet to be reflected in the data.

Economy-wide capex intentions are below average

AI theme helping to drive U.S. equity markets higher

With economic growth in the first half of the year predominantly being driven by accelerating AI investment, it’s no surprise then that the U.S. equity market has been led higher by those companies tied to this theme. A helpful way to look at this is through year-to-date earnings revisions. Earnings revisions have been most positive for utilities and financials. Given the dominance of the AI theme, it’s not surprising to see utilities revisions be comparatively strong as the need for further energy transmission capacity is ever-growing. Financials have benefited from a deregulatory push as well as an increase in deal-making activity. Revisions within the entire info tech complex have been mixed as investors weigh the possibility that AI will disrupt legacy software companies. Interestingly, AI is not necessarily a positive catalyst for the entire technology sector. At the opposite end, you have the largest downward revisions in segments such as consumer discretionary, which tend to be more exposed to tariffs and a slowing overall economy.

U.S. equity market and U.S. economy humming a similar tune

It seems that the U.S. equity market is reflecting the AI capex surge relative to more muted growth across the rest of the economy in the first half of the year. The question, of course, is whether this will continue, especially as it relates to the AI theme. Our view remains that the investment opportunities in the buildout of the AI ecosystem remain robust. Adoption has increased but remains generally low, and recent power-price auctions have shown an increased demand (and therefore higher price) for electricity, which underpins the need for further power generation and transmission investment. Going forward, it’s important to remember that the buildout has predominantly been concentrated in the U.S., but AI, of course, is a global theme that will need further development and presents opportunities outside the U.S. as well.

All market and economic data as of 09/03/2025 are sourced from Bloomberg Finance L.P. and FactSet unless otherwise stated.

You're invited to subscribe to our newsletters

We'll send you the latest market news, investing insights and more when you subscribe to our newsletters.

Global Investment Strategist